coming soon...the steward sheet : Your complete system to budget, save, invest, and eliminate debt — all in one simple, ultimate money manager for financial independence sign up below

How to Build an Emergency Fund in 2025: A Step-by-Step Guide

Building an emergency fund has become essential for financial security due to current economic uncertainty.

Liliane Meteumba

5/15/20253 min read

This guide will provide a step-by-step plan to create an emergency fund for 2025.

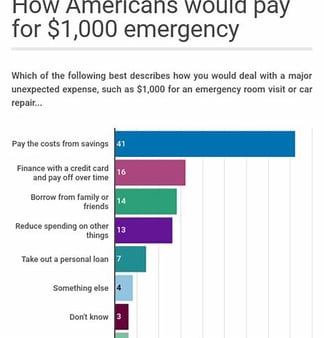

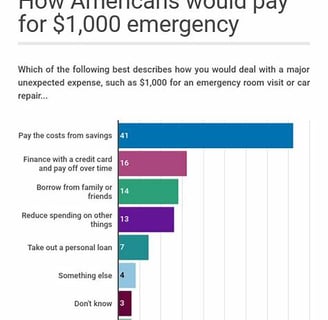

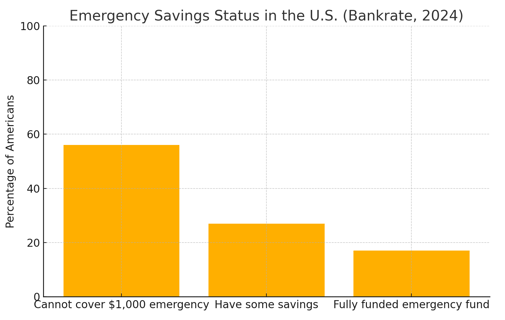

Building an emergency fund has become essential for financial security due to current economic uncertainty. The combination of fluctuating inflation rates with layoffs affecting multiple industries and increasing unexpected expenses leaves many Americans struggling to maintain financial stability. A 2024 Bankrate survey found that more than half of U.S. adults lack enough savings to handle a $1,000 emergency expense. A CNBC report from 2025 shows that emergency expenses drive Americans to incur high-interest credit card debt. This article presents an extensive step-by-step process for building a dependable emergency fund starting from zero.

Why an Emergency Fund Matters:

An emergency fund ensures financial stability when unexpected events such as job loss, medical bills or car repairs arise. People typically turn to credit cards or loans when they lack an emergency fund which results in prolonged debt accumulation. Experian's data reveals that by early 2025 the average credit card debt for Americans stands above $6,000. Proactive saving stands as the initial step toward preventing financial traps.

The Psychology of Saving:

An emergency fund helps people make better decisions while reducing their stress levels. Research from the American Psychological Association indicates that individuals who save money experience much less anxiety when facing emergencies. Financial peace of mind extends beyond numerical control to strengthen personal connections and boost both work efficiency and emotional health.

Step-by-Step Plan:

Set a Goal: Start small. Begin by saving $1,000 initially and work towards saving 3-6 months' worth of living expenses. Your budget helps you figure out the exact amount needed.

Track Your Expenses: Know where your money is going. Keep tabs on your spending by using free budgeting software such as Mint or YNAB along with your bank’s internal spending tracker to classify your expenditures.

Cut Non-Essentials:

-Review your discretionary spending.

-Eliminate subscriptions you don't use to save money and consider reducing your takeout orders along with reviewing your bills for possible renegotiation.

-The process of financial management automation can be simplified with the help of applications such as Trim and Truebill.

Automate Your Savings:

Establish an automatic transfer to a high-yield savings account either every week or month. Establish a weekly or monthly savings plan that transfers $10-$50 automatically to a high-yield savings account because consistent contributions matter more than the amount you save.

Use Windfalls Wisely:

Tax refunds, bonuses, or birthday cash? Put no less than 50% of any unexpected financial gain into your emergency savings account.

Visualize Your Progress:

A savings tracker or jar chart will help you maintain your motivation to save. Through gamification Qapital transforms saving practices into engaging activities which help users track their progress.

Economic Insight:

Because of the Federal Reserve's interest rate changes and economic growth forecasts until 2025 financial professionals advise single-income households to accumulate six months of emergency savings. Your emergency fund becomes increasingly essential because health insurance premiums and utility bills keep rising across multiple states.

Where to Park Your Emergency Fund:

Select accounts that provide easy access along with security features and interest earning capabilities.

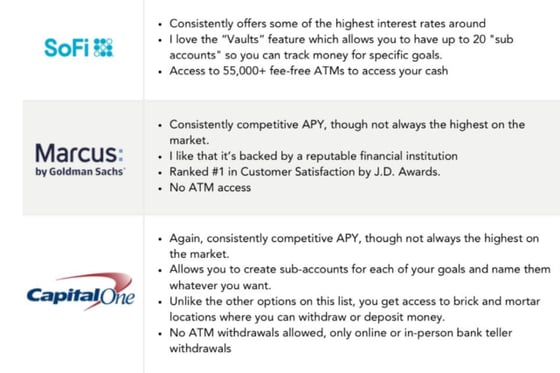

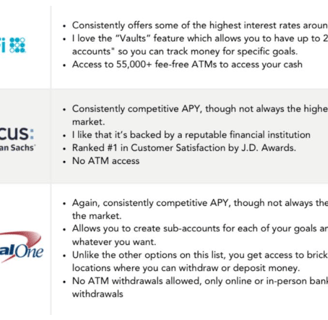

High-yield savings accounts: Ally, SoFi, Marcus by Goldman Sachs

Online banks and credit unions: Online banks and credit unions usually provide superior interest rates compared to traditional banks.

Avoid risky investments: The primary purpose of your emergency fund should be to provide financial security rather than to generate investment growth.

Avoid These Mistakes:

Misuse of your emergency fund for purposes other than emergencies such as vacations should be avoided.

Your emergency fund should not be kept in a checking account because it makes spending money too simple.

Not restoring money to your emergency fund after you withdraw from it.

Recommended HYSAs

Final Thoughts:

An emergency fund functions as both a financial safety buffer and a fundamental element of solid financial health and mental tranquility. Starting your savings early leads to greater financial security in your future. Begin your savings journey today instead of waiting for a crisis to highlight its importance.

Remember: Start small. Stay consistent. And let your discipline become your freedom.

Pass this article onto someone who should begin saving immediately.

SUSCRIBE on my YouTube channel @ https://www.youtube.com/@lilianemeteumba

Faith&Finance

Transform You finances without compromising your values!

757-301-1682

© 2025. All rights reserved.